样本外预测性能-R中的fGARCH

样本外预测性能-R中的fGARCH

提问于 2017-11-20 11:59:22

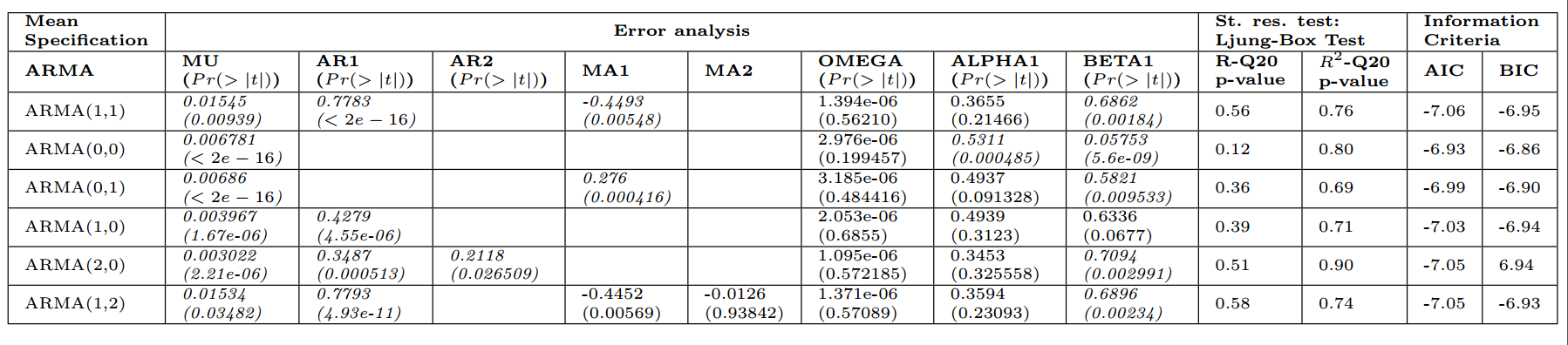

我分析了我的国内生产总值时间序列,以便作出预测。我发现最合适的模型是:

- GARCH(1,1)与ARMA (1,1):

garch1b<garchFit(~arma(1,1)+garch(1,1),data=dlogGDP,cond.dist="QMLE") - GARCH(1,1)与ARMA (1,0):

garch6b<garchFit(~arma(1,0)+garch(1,1),data=dlogGDP,cond.dist="QMLE")

GDP时间模式

两种模式都是有效的。我想做一个样本外预测性能比较.我使用了这个代码:

# Out-of-sample forcasting performance

y<-dlogGDP

S=round(0.75*length(y))

h=1

error1.h<-c()

for (i in S:(length(y)-h))

{

mymodel.sub<-garchFit(y[1:i], formula = ~arma(1,1)+garch(1,1))

predict.h<-predict(mymodel.sub,n.ahead=h)$pred[h]

error1.h<-c(error1.h,y[i+h]-predict.h)

}

error2.h<-c()

for (i in S:(length(y)-h))

{

mymodel.sub<-garchFit(y[1:i], formula = ~arma(1,0)+garch(1,1))

predict.h<-predict(mymodel.sub,n.ahead=h)$pred[h]

error2.h<-c(error2.h,y[i+h]-predict.h)

}

cbind(error1.h,error2.h)

# Mean Absolute Error

MAE1<-mean(abs(error1.h))

MAE2<-mean(abs(error2.h))

# Mean Squared Forcast Error

MAE1<-mean(abs(error1.h^2))

MAE2<-mean(abs(error2.h^2))

# Forcasting Performance Comparison

library(forecast)

dm.test(error1.h,error2.h,h=h,power=1)

dm.test(error1.h,error2.h,h=h,power=2)然而,我没有得到任何结果。error1.h和error2.h是NaN。

问题:

- 我的密码怎么了?

- 是否有另一种方法可以使用

fGARCH包( package )来进行非样例预测性能?

回答 1

Stack Overflow用户

发布于 2018-07-17 16:22:31

我认为,这只是缺少了一条关于预测输出的详细说明:

for (i in S:(length(y)-h))

{

mymodel.sub<-garchFit(y[1:i], formula = ~arma(1,0)+garch(1,1))

f <- fGarch::predict(mymodel.sub,n.ahead=h)

predict.h<-f$meanForecast

error1.h<-c(error1.h,y[i+h]-predict.h)

}页面原文内容由Stack Overflow提供。腾讯云小微IT领域专用引擎提供翻译支持

原文链接:

https://stackoverflow.com/questions/47391528

复制相关文章

相似问题

腾讯云开发者

Copyright © 2013 - 2026 Tencent Cloud. All Rights Reserved. 腾讯云 版权所有

深圳市腾讯计算机系统有限公司 ICP备案/许可证号:粤B2-20090059 ![]() 粤公网安备44030502008569号

粤公网安备44030502008569号

腾讯云计算(北京)有限责任公司 京ICP证150476号 | 京ICP备11018762号