时间序列数据的峰值到低谷

时间序列数据的峰值到低谷

提问于 2017-03-31 19:05:34

寻找一个股票指数的时间序列下降了10%或更大的每一个例子。我正在努力编写它的程序,以便它理解秩序的重要性(不希望升值10%)。

理想情况下,代码会:选择值,在值低于10%之后检查值,如果没有,检查下一步,继续检查,直到找到一个,然后记录下来。然后,移到“低谷”或“谷地”作为开始,在它比该值低10%或更多之后,继续检查它的值。

{kind=link}

{kind=link}

# Import Libraries

import pandas as pd

import numpy as np

import peakutils

from peakutils.plot import plot as pplot

from matplotlib import pyplot

import matplotlib.pyplot as plt

from scipy import signal

import csv

import scipy

import plotly.plotly as py

import plotly.graph_objs as go

from plotly.tools import FigureFactory as FF

# from pandas import DataFrame

# Import Excel as array

index = pd.read_csv(r"\Users\Reed_2\Desktop\Indexonly.csv")

print("as Pandas")

print (index.values)

# convert to 2 NumPy arrays

dates = index['Date'].as_matrix()

values = index['Index'].as_matrix()

print("values as NumPy")

print(values)

print("Date values")

print(dates)

# Find peaks

peaks = peakutils.indexes(values, thres=0.1, min_dist=1)

print ("peaks")

print(peaks)

a = np.asarray(peaks)

np.savetxt(r"C:\Users\Reed_2\Desktop\export.csv", a, delimiter=",")可以访问Python、R Studio和MatLab。我最喜欢Python。

非常感谢你在这方面的帮助。

回答 1

Stack Overflow用户

发布于 2017-03-31 19:31:25

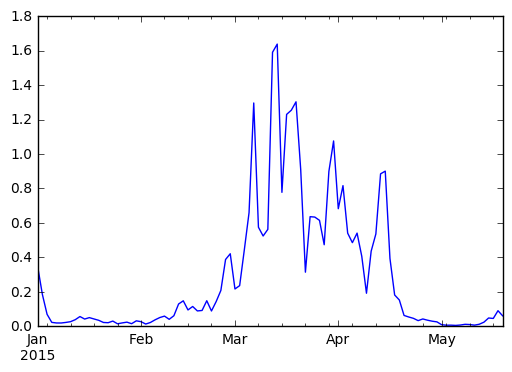

考虑一下返回的系列s

np.random.seed([3,1415])

s = pd.Series(

np.random.lognormal(.005, .5, size=100),

pd.date_range('2015-01-01', periods=100, freq='B')

).cumprod()

s.plot()

使用生成器将索引切片

def gen_slice(s, thresh):

sidx = s.index

idx = s.index[0]

v = s.get_value(idx)

yield idx

for idx in sidx[1:]:

v0 = s.get_value(idx)

if (v0 / v) < 1-thresh:

v = v0

yield idx

s.loc[list(gen_slice(s, .1))]

2015-01-01 0.346504

2015-01-02 0.184687

2015-01-05 0.069298

2015-01-06 0.022508

2015-01-07 0.018996

2015-01-26 0.014204

2015-02-03 0.012777

2015-05-01 0.008999

2015-05-04 0.006039

2015-05-06 0.004855

dtype: float64我们可以看到,每一个百分比的变化都小于10%。

s.loc[list(gen_slice(s, .1))].pct_change()

2015-01-01 NaN

2015-01-02 -0.467000

2015-01-05 -0.624783

2015-01-06 -0.675194

2015-01-07 -0.156034

2015-01-26 -0.252278

2015-02-03 -0.100442

2015-05-01 -0.295665

2015-05-04 -0.328967

2015-05-06 -0.195990

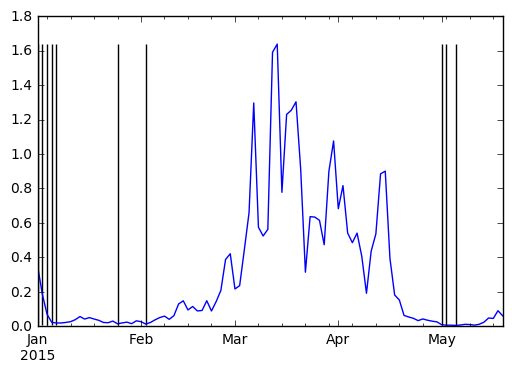

dtype: float64我们可以画出这些事件发生的地点。

idx = list(gen_slice(s, .1))

ax = s.plot()

ax.vlines(idx, s.min(), s.max())

另见下文:

可能有必要遍历一个系列的元素或数据帧的行,其方式是下一个元素或下一个行依赖于先前选定的元素或行。这称为路径依赖关系。

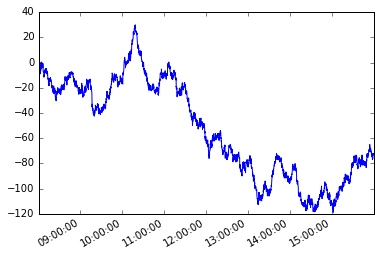

考虑以下不规则频率的时间序列s。

#starting python community conventions

import numpy as np

import pandas as pd

# n is number of observations

n = 5000

day = pd.to_datetime(['2013-02-06'])

# irregular seconds spanning 28800 seconds (8 hours)

seconds = np.random.rand(n) * 28800 * pd.Timedelta(1, 's')

# start at 8 am

start = pd.offsets.Hour(8)

# irregular timeseries

tidx = day + start + seconds

tidx = tidx.sort_values()

s = pd.Series(np.random.randn(n), tidx, name='A').cumsum()

s.plot();

让我们假设路径依赖条件。从该系列的第一个成员开始,我希望获取每个后续元素,以便该元素与当前元素之间的绝对差异大于或等于x。

我们将使用python生成器解决这个问题。

生成器函数

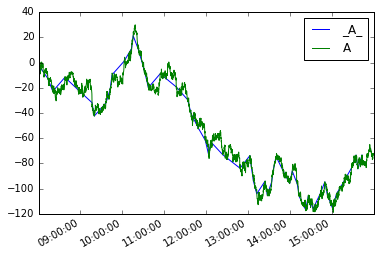

def mover(s, move_size=10):

"""Given a reference, find next value with

an absolute difference >= move_size"""

ref = None

for i, v in s.iteritems():

if ref is None or (abs(ref - v) >= move_size):

yield i, v

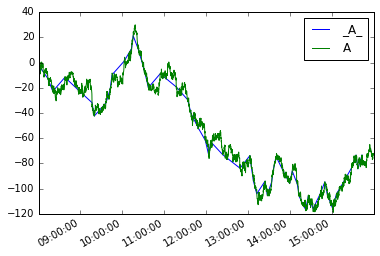

ref = v然后我们就可以定义一个新的系列moves,如下所示

moves = pd.Series({i:v for i, v in mover(s, move_size=10)},

name='_{}_'.format(s.name))把他们都画出来

moves.plot(legend=True)

s.plot(legend=True)

数据文件的模拟将是:

def mover_df(df, col, move_size=2):

ref = None

for i, row in df.iterrows():

if ref is None or (abs(ref - row.loc[col]) >= move_size):

yield row

ref = row.loc[col]

df = s.to_frame()

moves_df = pd.concat(mover_df(df, 'A', 10), axis=1).T

moves_df.A.plot(label='_A_', legend=True)

df.A.plot(legend=True)

页面原文内容由Stack Overflow提供。腾讯云小微IT领域专用引擎提供翻译支持

原文链接:

https://stackoverflow.com/questions/43147940

复制相关文章

相似问题

腾讯云开发者

Copyright © 2013 - 2026 Tencent Cloud. All Rights Reserved. 腾讯云 版权所有

深圳市腾讯计算机系统有限公司 ICP备案/许可证号:粤B2-20090059 ![]() 粤公网安备44030502008569号

粤公网安备44030502008569号

腾讯云计算(北京)有限责任公司 京ICP证150476号 | 京ICP备11018762号