对所有分类变量的系数都有差异的模型,得到“对比编码”来做到这一点?

假设我们想做一个简单的“收入描述模型”。假设我们有三个组,北、中、南(想想美国地区)。与其他类似群体相比,假设北方地区的平均收入为130人,中部地区为80人,南方为60人。假设组大小相等,那么平均值是90。

在(线性回归)模型中,应该有一种方法将系数报告为与总体均值不同的方法(在多元上下文中,“所有其他相等的”),并为每一种方法得到一个:

$\beta_{North} =40美元

$\beta_{Central} =-10美元

$\beta_{South} =-30美元

很明显跳过了拦截。

对我来说这似乎是最直观的。但我一辈子都想不出如何用R的“对比编码”来得到这个。(而且,这似乎会把变量名搞砸)。

为我的模拟/mwe设定参数

m_inc <- 90

b_n <- 40

b_c <- -10

b_s <- -30

sd_prop <- 0.5 #sd as share of mean

pop_per <- 1000 模拟数据

set.seed(100)

n_income <- rnorm(pop_per, m_inc + b_n, (m_inc + b_n)*sd_prop)

c_income <- rnorm(pop_per, m_inc + b_c, (m_inc + b_s)*sd_prop)

s_income <- rnorm(pop_per, m_inc + b_s, (m_inc + b_s)*sd_prop)

noise_var <- rnorm(pop_per*3, 0, (m_inc + b_s)*sd_prop)

i_df <- tibble(

region = rep( c("n", "c", "s"), c(pop_per, pop_per, pop_per) ),

income = c(n_income, c_income, s_income),

noise_var

) %>%

mutate(region = as.factor(region))

i_df %>% # Summary by group using purrr

split(.$region) %>%

purrr::map(summary)看上去够近了。

现在我想用“模型收入”来检验按地区“控制其他因素”的差异。为了说明这个问题,让我们把南方作为基础。我设置了默认的contr.treatment,以防您重置它。

i_df <- i_df %>% mutate(region = relevel(region, ref="s"))

options(contrasts = rep ("contr.treatment", 2))

(

basic_lm <- i_df %>% lm(income ~ region + noise_var, .)

)标准的事情是:截距(大约)是‘基组’的平均值,南部,系数regionc和regionn代表这些,大约+20和+70的相对调整。

这是标准的“虚拟编码”,即“处理编码”,默认的is。

我们可以将这个默认值(对于无序变量)调整为无序和有序的“和对比度编码”。

options(contrasts = rep ("contr.sum", 2))

(

basic_lm_cc <- i_df %>% lm(income ~ region + noise_var, .)

)现在,这似乎得到了我们正在寻找的调整系数,但是

,

- ,这些区域的名称丢失了;我怎么知道哪个是哪一个?

- ,它显然是在报告s(南部)和c(中部)的调整系数。不太直观。

无论我们如何重新划分该地区以设置一个特定的基地组(我尝试过),情况似乎都是如此.系数不变。

我找到了解决办法,但这不是“正确的方法”。I非指结果(收入)变量,并强制0截距:

i_df %>%

mutate(m_inc = mean(income)) %>%

lm(income - m_inc ~ 0 + region + noise_var, .)耶!这就是我想要的,神奇的是,变量名被保留了下来。但这似乎是个奇怪的方法。还请注意,使用上述代码,无论是和还是处理,这组系数都会出现。

如何使用对比编码或其他工具“正确的方式”完成这一任务?

回答 1

Stack Overflow用户

发布于 2022-07-06 07:21:52

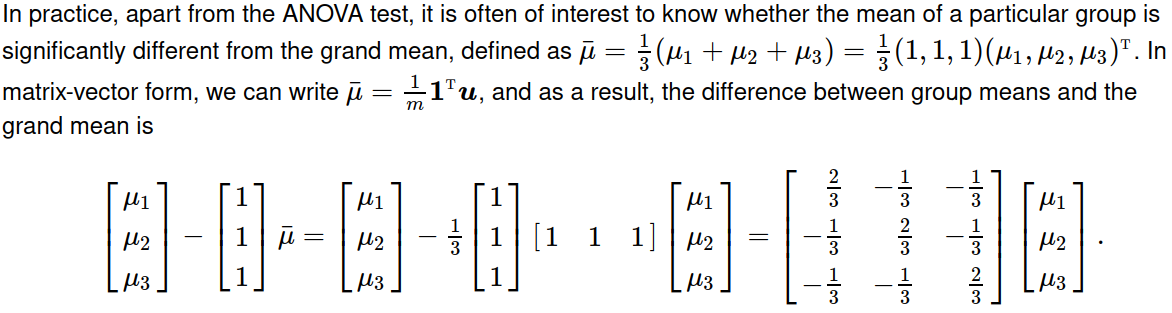

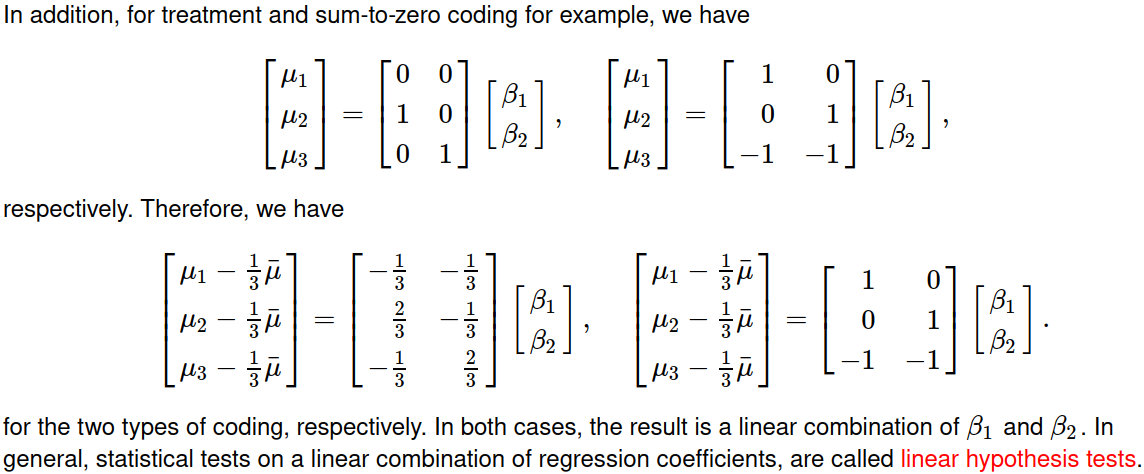

我们不能通过对比编码来达到这个目的。在单向方差分析中,对比被用来将N级因子编码为N1变量,再加上一个截距,所以N个变量仍然是N个变量。但是,在模型中同时考虑群均值的大均值和偏差,是从N个变量到N+1变量的再参数化。这(即使我们找到了一种方法)使得设计矩阵缺乏秩,而lm/aov/glm,等则会将一个变量放入NA。

一般来说,我们必须做后续的统计分析.在这个答案中,我将总结编码的不同之处,并以四种方式说明如何比较组均值和大平均值:使用multcomp、 this 和car进行编码。

library(ggplot2)

library(car)

library(multcomp)

library(emmeans)设置

我要用一个和你相似的例子。

SimData <- function (group.size, group.mean, group.variance) {

## number of groups

ng <- length(group.size)

if (ng > 5) stop("There is no need to experiment that many groups!")

## number of observations per group

n <- sum(group.size)

## generate a factor variable 'f' for these groups

f <- rep.int(factor(sprintf("G%d", 1:ng)), group.size)

## simulate samples from each group

mu <- rep.int(group.mean, group.size)

se <- rep.int(sqrt(group.variance), group.size)

y <- rnorm(n, mu, se)

## numerical covariate 'x' with slope = 1

lim <- sd(y)

br <- seq.int(-lim, lim, length.out = ng + 1)

interval <- cbind(br[-(ng + 1)], br[-1])

interval <- interval[sample.int(ng), ]

a <- rep.int(interval[, 1], group.size)

b <- rep.int(interval[, 2], group.size)

x <- runif(n, a, b)

## create data.frame

data.frame(y = y + x, f = f, x = x)

}

set.seed(4891738) ## my Stack Overflow ID

group.size <- c(100, 125, 150)

group.mean <- c(130, 80, 60)

group.variance <- 0.25 * group.mean

dat <- SimData(group.size, group.mean, group.variance)

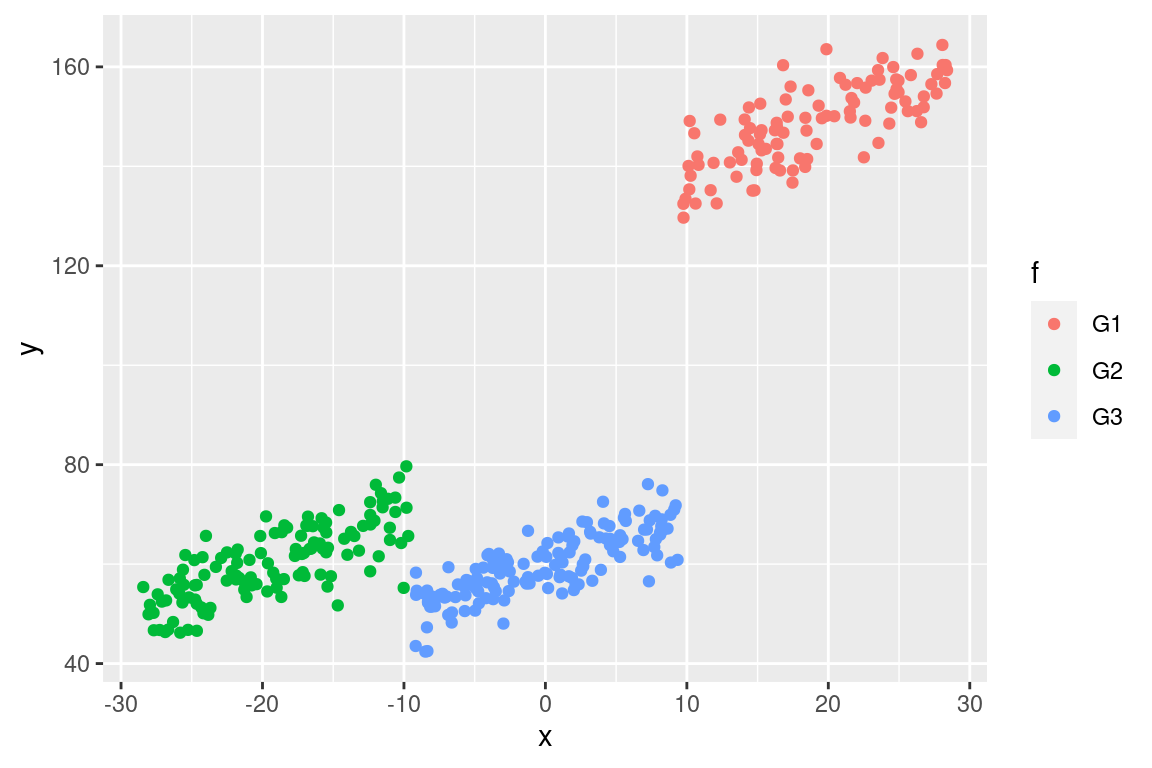

ggplot(data = dat, mapping = aes(x = x, y = y, colour = f)) + geom_point()

对每一组的均值和方差进行天真的计算是有误导性的,因为我们离事实很远!

## true values are 130, 80, 60

with(dat, tapply(y, f, mean))

## G1 G2 G3

## 148.36985 60.38273 59.45486

## true values are 32.5, 20 and 15

with(dat, tapply(y, f, var))

## G1 G2 G3

## 67.37108 55.25185 41.69867对比编码

## treatment coding

contr.treatment(3)

## 2 3

## 1 0 0

## 2 1 0

## 3 0 1

## sum-to-zero coding

contr.sum(3)

## [,1] [,2]

## 1 1 0

## 2 0 1

## 3 -1 -1

fit.treatment <- lm(y ~ f + x, dat, contrasts = list(f = "contr.treatment"))

coef(fit.treatment)

#(Intercept) fG2 fG3 x

# 128.94609 -48.71525 -69.03433 1.03121

summary(fit.treatment)

anova(fit.treatment)

fit.sum <- lm(y ~ f + x, dat, contrasts = list(f = "contr.sum"))

coef(fit.sum)

#(Intercept) f1 f2 x

# 89.696234 39.249860 -9.465391 1.031210

summary(fit.sum)

anova(fit.sum)请注意,虽然使用不同的对比编码给出不同的回归系数,但它们实际上是等价的,产生相同的拟合值。

all.equal(fit.treatment$fitted.values, fit.sum$fitted.values)

## [1] TRUE将群体均值与均数进行比较

R中的线性假设检验

1.无花式包的香草方法()

## 3 x 2 linear combination matrix

wt.treatment <- matrix(c(-1, 2, -1, -1, -1, 2), nrow = 3) / 3

wt.sum <- matrix(c(1, 0, -1, 0, 1, -1), nrow = 3)

vanilla <- function (wt, beta.ind, lmfit) {

## beta coefficients and their covariance matrix

beta <- coef(lmfit)[beta.ind]

V <- vcov(lmfit)[beta.ind, beta.ind]

## linear combination and their standard errors

MEAN <- c(wt %*% beta)

## get standard errors for sum of `LinearComb`

SE <- sqrt(diag(wt %*% tcrossprod(V, wt)))

## perform t-test

tscore <- MEAN / SE

pvalue <- 2 * pt(abs(tscore), lmfit$df.residual, lower.tail = FALSE)

## return a matrix

ans <- matrix(c(MEAN, SE, tscore, pvalue), ncol = 4L)

colnames(ans) <- c("Estimate", "Std. Error", "t value", "Pr(>|t|)")

printCoefmat(ans)

}

vanilla(wt.treatment, 2:3, fit.treatment)

## Estimate Std. Error t value Pr(>|t|)

## [1,] 39.24986 0.90825 43.215 < 2.2e-16 ***

## [2,] -9.46539 0.89404 -10.587 < 2.2e-16 ***

## [3,] -29.78447 0.32466 -91.741 < 2.2e-16 ***

## ---

## Signif. codes: 0 '***' 0.001 '**' 0.01 '*' 0.05 '.' 0.1 ' ' 1

vanilla(wt.sum, 2:3, fit.sum) ## identical to above2.使用包“multcomp”

## pad columns of zeros to zero out the effect of alpha and gamma

wt.treatment0 <- cbind(0, wt.treatment, 0)

wt.sum0 <- cbind(0, wt.sum, 0)

summary(glht(fit.treatment, linfct = wt.treatment0))

## Linear Hypotheses:

## Estimate Std. Error t value Pr(>|t|)

## 1 == 0 39.2499 0.9083 43.22 <2e-16 ***

## 2 == 0 -9.4654 0.8940 -10.59 <2e-16 ***

## 3 == 0 -29.7845 0.3247 -91.74 <2e-16 ***

## ---

## Signif. codes: 0 '***' 0.001 '**' 0.01 '*' 0.05 '.' 0.1 ' ' 1

## (Adjusted p values reported -- single-step method)

summary(glht(fit.sum, linfct = wt.sum0)) ## identical to above3.使用软件包‘emmeans’

emmeans(fit.treatment, specs = eff ~ f)

## $emmeans

## f emmean SE df lower.CL upper.CL

## G1 127.3 1.002 371 125.4 129.3

## G2 78.6 0.874 371 76.9 80.3

## G3 58.3 0.379 371 57.5 59.0

##

## Confidence level used: 0.95

##

## $contrasts

## contrast estimate SE df t.ratio p.value

## G1 effect 39.25 0.908 371 43.215 <.0001

## G2 effect -9.47 0.894 371 -10.587 <.0001

## G3 effect -29.78 0.325 371 -91.741 <.0001

##

## P value adjustment: fdr method for 3 tests

emmeans(fit.sum, specs = eff ~ f) ## identical to above在这里,使用specs = ~f或specs = "f",只报告$emmeans (边缘均值)组件。左手边的"eff“表示要调用eff.emmc()来应用对比,而$contrasts组件提供了这样的结果。

4.使用软件包“car”

linearHypothesis()函数来自cars,执行F-测试,以测试所有线性组合是否同时为0。因此,它不同于上面演示的t检验。此外,它还产生了错误:

linearHypothesis(fit.treatment, hypothesis.matrix = wt.treatment0)

#Error in solve.default(vcov.hyp) :

# system is computationally singular: reciprocal condition number = 1.12154e-17

linearHypothesis(fit.sum, hypothesis.matrix = wt.sum0) ## identical to above从某种意义上说,这个答案是我以前几个答案的总结。

https://stackoverflow.com/questions/67495319

复制相似问题

腾讯云开发者

Copyright © 2013 - 2026 Tencent Cloud. All Rights Reserved. 腾讯云 版权所有

深圳市腾讯计算机系统有限公司 ICP备案/许可证号:粤B2-20090059 ![]() 粤公网安备44030502008569号

粤公网安备44030502008569号

腾讯云计算(北京)有限责任公司 京ICP证150476号 | 京ICP备11018762号