使用Gekko发布敏感性报告

使用Gekko发布敏感性报告

提问于 2020-09-17 15:13:35

我用Gekko来解决一个简单的线性规划问题。我得到了一个最优解。当我试图获得敏感性报告时,我将面临以下错误。

@error: Degrees of Freedom Non-Zero for Sensitivity Analysis然而,当我在excel中尝试同样的方法时,我没有看到任何问题。请帮我找出问题的确切原因。

问题陈述:

from gekko import GEKKO

model = GEKKO(remote=False)

model.options.SENSITIVITY = 1 # sensitivity analysis

model.options.SOLVER = 1 # change solver (1=APOPT, 3=IPOPT)

#Maximum demand and implicit contraints as upper bound and lower bound

x1 = model.Var(lb=0, ub=50) # Product DH

x2 = model.Var(lb=0, ub=20) # Product TH

#Objective function

model.Maximize(45*x1+50*x2) # Profit function

#Constraints

model.Equation(500*x1+500*x2<=20000) #Cornflour

model.Equation(750*x1+625*x2<=42000) #Sugar

model.Equation(150*x1+100*x2<=10400) #Fruit and Nut

model.Equation(200*x1+300*x2<=9600) #Ghee

model.solve(disp=True, debug = 1)

p1 = x1.value[0]; p2 = x2.value[0]

print ('Product 1 (DH) in Kgs: ' + str(p1))

print ('Product 2 (TH) in Kgs: ' + str(p2))

print ('Profit : Rs.' + str(45*p1+50*p2))

print(model.path)下面是带有错误的代码输出:

---------------------------------------------------

Solver : APOPT (v1.0)

Solution time : 0.0489 sec

Objective : -1880.

Successful solution

---------------------------------------------------

Generating Sensitivity Analysis

Number of state variables: 6

Number of total equations: - 4

Number of independent FVs: - 0

Number of independent MVs: - 0

---------------------------------------

Degrees of freedom : 2

Error: DOF must be zero for sensitivity analysis

@error: Degrees of Freedom Non-Zero for Sensitivity Analysis

Writing file sensitivity_dof.t0

STOPPING...回答 1

Stack Overflow用户

回答已采纳

发布于 2020-09-18 00:04:37

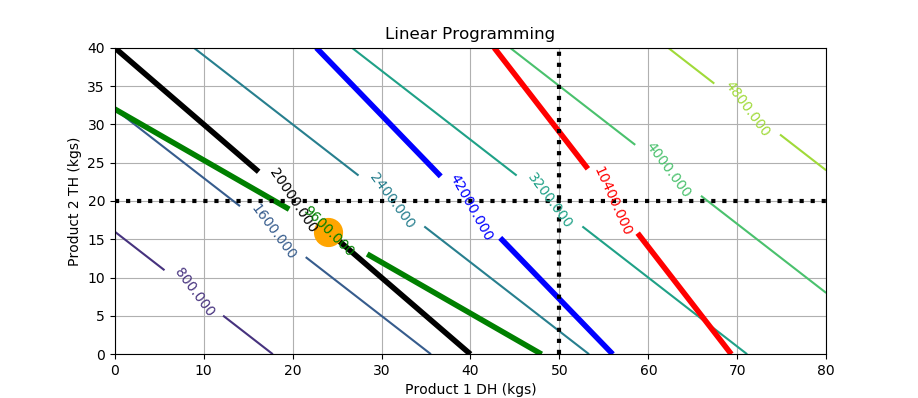

Gekko需要相同数量的变量和约束来执行灵敏度分析。它只适用于正方形系统,在那里你试图理解模型的输入和输出之间的关系。也许您需要的是约束的影子价格,而不是灵敏度分析。因为您的问题只有两个变量,所以您可以使用等高线图来可视化约束和目标。

from gekko import GEKKO

model = GEKKO(remote=False)

model.options.SENSITIVITY = 0 # sensitivity analysis

model.options.SOLVER = 1 # change solver (1=APOPT,3=IPOPT)

#Maximum demand and implicit contraints as upper bound and lower bound

x1 = model.Var(lb=0, ub=50) # Product DH

x2 = model.Var(lb=0, ub=20) # Product TH

#Objective function

model.Maximize(45*x1+50*x2) # Profit function

#Constraints

model.Equation(500*x1+500*x2<=20000) #Cornflour

model.Equation(750*x1+625*x2<=42000) #Sugar

model.Equation(150*x1+100*x2<=10400) #Fruit and Nut

model.Equation(200*x1+300*x2<=9600) #Ghee

model.solve(disp=True, debug = 1)

p1 = x1.value[0]; p2 = x2.value[0]

print ('Product 1 (DH) in Kgs: ' + str(p1))

print ('Product 2 (TH) in Kgs: ' + str(p2))

print ('Profit : Rs.' + str(45*p1+50*p2))

print(model.path)

## Generate a contour plot

# Import some other libraries that we'll need

# matplotlib and numpy packages must also be installed

import matplotlib

import numpy as np

import matplotlib.pyplot as plt

# Design variables at mesh points

x1 = np.arange(0.0, 81.0, 2.0)

x2 = np.arange(0.0, 41.0, 2.0)

x1, x2 = np.meshgrid(x1,x2)

# Equations and Constraints

cf = 500*x1+500*x2

sg = 750*x1+625*x2

fn = 150*x1+100*x2

gh = 200*x1+300*x2

# Objective

obj = 45*x1+50*x2

# Create a contour plot

plt.figure()

# Weight contours

CS = plt.contour(x1,x2,obj)

plt.clabel(CS, inline=1, fontsize=10)

# Constraints

CS = plt.contour(x1, x2, cf,[20000],colors='k',linewidths=[4.0])

plt.clabel(CS, inline=1, fontsize=10)

CS = plt.contour(x1, x2, sg,[42000],colors='b',linewidths=[4.0])

plt.clabel(CS, inline=1, fontsize=10)

CS = plt.contour(x1, x2, fn,[10400],colors='r',linewidths=[4.0])

plt.clabel(CS, inline=1, fontsize=10)

CS = plt.contour(x1, x2, gh,[9600],colors='g',linewidths=[4.0])

plt.clabel(CS, inline=1, fontsize=10)

# plot optimal solution

plt.plot(p1,p2,'o',color='orange',markersize=20)

# plot bounds

plt.plot([0,80],[20,20],'k:',lw=3)

plt.plot([50,50],[0,40],'k:',lw=3)

# Add some labels

plt.title('Linear Programming')

plt.xlabel('Product 1 DH (kgs)')

plt.ylabel('Product 2 TH (kgs)')

plt.grid()

plt.savefig('contour.png')

plt.show()编辑:检索影子价格(拉格朗日乘数)

拉格朗日乘数(影子价格)可用于约束时,您使用IPOPT求解器。将m.options.SOLVER=3设置为IPOPT,并将诊断级别设置为2+和m.options.DIAGLEVEL=2。下面是用于生成影子价格的修改代码:

from gekko import GEKKO

model = GEKKO(remote=False)

model.options.DIAGLEVEL = 2

model.options.SOLVER = 3 # change solver (1=APOPT,3=IPOPT)

#Maximum demand and implicit contraints as upper bound and lower bound

x1 = model.Var(lb=0, ub=50) # Product DH

x2 = model.Var(lb=0, ub=20) # Product TH

#Objective function

model.Maximize(45*x1+50*x2) # Profit function

#Constraints

model.Equation(500*x1+500*x2<=20000) #Cornflour

model.Equation(750*x1+625*x2<=42000) #Sugar

model.Equation(150*x1+100*x2<=10400) #Fruit and Nut

model.Equation(200*x1+300*x2<=9600) #Ghee

model.solve(disp=True, debug = 1)

p1 = x1.value[0]; p2 = x2.value[0]

print ('Product 1 (DH) in Kgs: ' + str(p1))

print ('Product 2 (TH) in Kgs: ' + str(p2))

print ('Profit : Rs.' + str(45*p1+50*p2))

# for shadow prices, turn on DIAGLEVEL to 2+

# and use IPOPT solver (APOPT doesn't export Lagrange multipliers)

# Option 1: open the run folder and open apm_lam.txt

model.open_folder()

# Option 2: read apm_lam.txt into array

import numpy as np

lam = np.loadtxt(model.path+'/apm_lam.txt')

print(lam)结果是:

Product 1 (DH) in Kgs: 24.0

Product 2 (TH) in Kgs: 16.0

Profit : Rs.1880.0

[-6.99999e-02 -3.44580e-11 -1.01262e-10 -5.00000e-02]页面原文内容由Stack Overflow提供。腾讯云小微IT领域专用引擎提供翻译支持

原文链接:

https://stackoverflow.com/questions/63941113

复制相关文章

相似问题

腾讯云开发者

Copyright © 2013 - 2026 Tencent Cloud. All Rights Reserved. 腾讯云 版权所有

深圳市腾讯计算机系统有限公司 ICP备案/许可证号:粤B2-20090059 ![]() 粤公网安备44030502008569号

粤公网安备44030502008569号

腾讯云计算(北京)有限责任公司 京ICP证150476号 | 京ICP备11018762号